FLA Return Filing in India: Applicability, Due Date, and Penalties

The Foreign Liabilities and Assets (FLA) return is one of those compliance obligations that companies discover they have been missing for years, usually when an investor’s legal team raises it during due diligence or when a compounding application needs to be filed before a transaction can close.

FLA return filing in India is a mandatory annual requirement under the Foreign Exchange Management Act, 1999. It is not a transaction-specific filing. It does not depend on whether any new investment was received during the year. If a company has outstanding foreign investment on its balance sheet as of March 31, the FLA return must be filed. Every year. Until the foreign investment is fully repatriated or the company is wound up.

This blog covers who must file, what must be reported, the due date, the consequences of non-filing, and the most common mistakes companies make.

What is the FLA Return and Why Is It Required?

The FLA return is an annual survey mandated by the Reserve Bank of India under FEMA, 1999, to capture India’s foreign liabilities and assets position. It is submitted to RBI’s Department of Statistics and Information Management (DSIM) and forms part of India’s Balance of Payments and International Investment Position statistics.

The Foreign Liabilities and Assets Return India requirement was introduced to give RBI a comprehensive, annually updated picture of how much foreign capital is invested in Indian companies and how much Indian capital is invested abroad. It covers both sides: foreign investment received by Indian companies (foreign liabilities) and investments made by Indian companies overseas (foreign assets).

The data collected through FLA return filing in India feeds directly into RBI’s annual External Sector Statistics and India’s reporting to international bodies including the IMF. This is why RBI treats non-filing seriously. It is not a paperwork formality. It is a data submission that RBI uses for policy analysis and international reporting.

Who Must File the FLA Return in India?

Every Indian company and LLP that has received Foreign Direct Investment or made Overseas Direct Investment, and has outstanding foreign investment or overseas investment on its balance sheet as of March 31, must file the FLA return.

The applicability is broader than most companies realise. The key points:

Indian companies that have received FDI: If a company received foreign investment in any previous year and that investment is still outstanding on the balance sheet as of March 31 of the current year, the FLA return must be filed even if no new FDI was received during the year.

Indian companies that have made ODI: If an Indian company has an outstanding Overseas Direct Investment in a foreign subsidiary or joint venture as of March 31, the FLA return must be filed.

LLPs: FLA return filing in India applies to LLPs that have received FDI or made ODI, not just companies.

Who is exempt: Indian companies that have not received any FDI and have not made any ODI, and have no outstanding foreign investment of any kind on their balance sheet as of March 31, are not required to file.

The most common mistake here is a company that received FDI three years ago, has made no new transactions since, and assumes the FLA obligation lapsed. It did not. The filing obligation continues as long as the foreign investment is outstanding.

What Must Be Reported in FLA Return Filing in India?

The FLA return captures the company’s foreign liabilities and foreign assets as of March 31 of the reporting year, along with income flows during the year.

The return is filed online through RBI’s FLAIR (Foreign Liabilities and Assets Information Reporting) portal at flair.rbi.org.in. The filing requires audited or provisional financial data depending on the filing timeline.

Key information reported includes:

Foreign Liabilities:

- FDI received by the Indian company: equity, reinvested earnings, and other capital

- External commercial borrowings outstanding

- Trade credit outstanding

- Foreign portfolio investment (if applicable)

Foreign Assets:

- ODI made by the Indian company: equity in foreign subsidiaries and JVs

- Loans extended to foreign entities

- Guarantees issued on behalf of overseas entities

Income Flows:

- Dividends paid to foreign investors during the year

- Interest paid on ECBs

- Dividends received from overseas investments

For companies with audited accounts finalised before the due date, audited figures must be used. For companies whose accounts are not yet audited by the due date, provisional (unaudited) figures must be submitted and revised later if the audited figures differ materially.

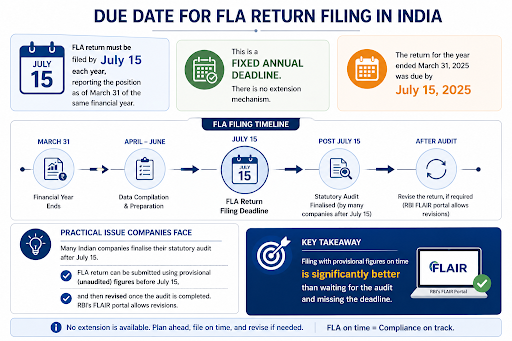

What is the Due Date for FLA Return Filing in India?

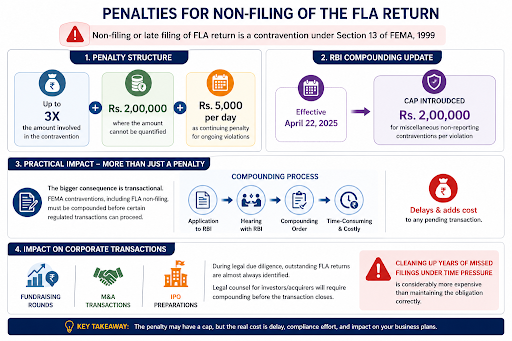

What Are the Penalties for Non-Filing of the FLA Return?

What Are the Most Common Mistakes in FLA Return Filing in India?

The failures in FLA return filing in India follow a consistent pattern and almost none of them involve complex legal questions.

Assuming no new transaction means no filing: As discussed, the FLA obligation does not depend on new transactions. It depends on outstanding foreign investment. Companies that received FDI years ago and have made no transactions since are still required to file annually.

Missing the July 15 deadline because the audit is not complete: One of the recurring issues in FLA Return Filing in India is delaying the filing until the audit is completed. The correct approach is to submit provisional figures before July 15 and revise them later if needed. Missing the deadline altogether leads to a compoundable contravention.

Not reporting ODI: Similarly, companies often fail to report ODI. Any Indian company with overseas subsidiaries must include its ODI details in the FLA return, even though many tend to focus only on FDI.

Using incorrect financial data: The FLA return requires specific balance sheet line items. Companies that use consolidated figures when standalone figures are required, or that convert foreign currency balances at the wrong rate, create discrepancies that generate regulatory queries.

Registering on the wrong portal: The FLA return is filed through RBI’s FLAIR portal at flair.rbi.org.in. It is not filed through the FIRMS portal, which handles FC-GPR and FC-TRS. Companies that confuse the two portals create delays in the filing process.

Conclusion

FLA return filing in India is an annual obligation that runs for the entire life of the foreign investment. It does not expire, it does not self-complete, and it cannot be deferred without creating a compoundable FEMA contravention. The July 15 deadline is fixed, the provisional filing option is available, and there is no operational reason to miss it.

CorporateLegit handles FLA return filing in India for companies with outstanding FDI and ODI positions, including companies with multiple years of missed filings that require compounding before a pending transaction can proceed. If your company has received foreign investment or made overseas investments and has not been maintaining its FLA filings, reach out to CorporateLegit to assess the compliance position before your next transaction.

FAQ

- What is the FLA return and who needs to file it?

The FLA return is an annual survey mandated by RBI under FEMA, 1999, capturing a company’s foreign liabilities and assets as of March 31. Any Indian company or LLP with outstanding FDI received or ODI made, as of March 31, must file the return by July 15 each year, regardless of whether any new transactions occurred during the year. - What is the due date for FLA return filing in India?

The FLA return must be filed by July 15 each year for the position as of March 31 of the same financial year. There is no extension. Companies whose audits are not complete by July 15 must file using provisional figures and revise once the audit is finalised. - What is the penalty for missing the FLA return deadline?

Non-filing is a FEMA contravention under Section 13, attracting penalties of up to three times the amount involved, or Rs. 2 lakh where the amount cannot be quantified, plus Rs. 5,000 per day for continuing violations. Under RBI’s revised compounding framework (April 2025), a Rs. 2,00,000 cap applies to miscellaneous non-reporting contraventions. Compounding requires a formal RBI application and hearing. - Is the FLA return required if no new FDI was received during the year?

Yes. The filing obligation is based on outstanding foreign investment as of March 31, not on new transactions during the year. A company that received FDI five years ago and has made no subsequent transactions must still file the FLA return annually as long as the investment remains outstanding. - Where is the FLA return filed?

The FLA return is filed online through RBI’s FLAIR portal at flair.rbi.org.in. It is separate from the FIRMS portal, which handles FC-GPR and FC-TRS filings. The entity must register on the FLAIR portal and submit the return using the applicable reporting format for companies or LLPs. - Does the FLA return cover Overseas Direct Investment as well?

Yes. Indian companies with outstanding ODI in foreign subsidiaries or joint ventures must report their foreign assets position in the FLA return. This includes equity invested in foreign entities, loans extended to overseas entities, and guarantees issued on behalf of overseas subsidiaries. The FLA return captures both inbound and outbound foreign investment positions.