Strategic Demergers in India: Process, Legal Framework, and Value Unlocking

Corporate growth takes different forms. Separation is one of them, and often the more valuable one. For Indian conglomerates and multinational subsidiaries, carving out a business unit into an independent entity often creates more value than keeping everything under one roof. That is what strategic demergers in India are built around. The concept has been around for a while. The regulatory environment surrounding it has not. The Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025, notified by the Ministry of Corporate Affairs on 4th September 2025, have redrawn how demergers can be approached in India. Businesses considering this path need to understand where the framework stands and what changed on 4th September 2025.

What Exactly Is a Strategic Demerger in India?

Under Section 2(19AA) of the Income Tax Act, 1961, a demerger is the transfer of one or more undertakings from the Demerged Company to a Resulting Company through a court-approved scheme of arrangement. Shareholders of the Demerged Company receive shares in the Resulting Company in proportion to what they already hold. No cash changes hands in the process.

There is a specific commercial logic at play here. Unrelated business lines sitting under one entity tend to get undervalued by the market. Each business, priced independently, often commands a higher valuation than its contribution to the consolidated group. Demerging solves what practitioners call the conglomerate discount problem.

Tata Motors is the most current example. Following NCLT approval from the Mumbai bench in August 2025, its commercial vehicle business is being separated into a new entity called TML Commercial Vehicles Limited. Passenger vehicles and Jaguar Land Rover operations stay in the parent. The scheme was approved under Sections 230 to 232 of the Companies Act, 2013, with 99.99% shareholder approval. Shareholder approval at that level does not happen by default. It points to how well the commercial rationale was laid out and communicated.

What Is the Legal Framework Governing Strategic Demergers in India?

Strategic demergers in India do not sit within a single regulatory framework. The Companies Act, the Income Tax Act, SEBI regulations, and FEMA all apply, and none of them wait for the others. Each has to be worked through at the same time.

Companies Act, 2013 — Sections 230 to 232

Sections 230 to 232 form the backbone of any scheme of arrangement. Section 232 is where NCLT’s powers in sanctioning demergers are specifically addressed.

Section 233, Companies Act, 2013

Eligible companies can bypass the NCLT entirely under this provision. The demerger goes through the Regional Director instead, which is faster and considerably less expensive.

CAA Rules, 2016 and CAA Amendment Rules, 2025

The procedural framework for scheme filings, timelines, and forms. What the 2025 amendment did was widen the fast-track eligibility net in a way that makes the route accessible to companies that had no practical alternative to the NCLT process before.

Section 2(19AA) and Section 47, Income Tax Act, 1961

Section 2(19AA) draws the line between what qualifies as a demerger and what does not. Section 47 is where the tax-neutral treatment conditions sit.

SEBI (LODR) Regulations, 2015 and SEBI Master Circular on Schemes of Arrangement

Listed companies have an additional layer to deal with. Both the LODR Regulations and the Master Circular dated 20th June 2023 apply to any listed company going through a demerger.

FEMA, 1999 and NDI Rules, 2019

Foreign shareholding in either the demerged or resulting entity brings FEMA and the NDI Rules into the picture.

What Are the Main Types of Strategic Demergers in India?

The type of demerger depends on the business structure and what is being separated. Four categories cover most transactions.

Vertical Demerger

Different business verticals are separated into independent entities. Each resulting company operates in its own sector, with its own management and capital structure.

Horizontal Demerger

Division based on geography or product category, where the separated units operate in parallel markets rather than stacked verticals.

Subsidiary Demerger

A holding company moves a portion of its business to an existing or newly formed subsidiary. The effect is that the transferred business sits behind its own balance sheet, separated from the parent’s liabilities.

Inbound Cross-Border Demerger

A foreign holding company transfers a business undertaking to its Indian subsidiary. The outbound equivalent, where an Indian company transfers an undertaking to a foreign entity, remains legally ambiguous. The Foreign Exchange Management (Cross Border Merger) Regulations, 2018, omitted the term “demerger” entirely, and that gap has not been legislatively resolved. Anyone evaluating an outbound cross-border demerger needs specific legal advice on the FEMA implications before proceeding.

What Is the Step-by-Step Process for Strategic Demergers in India?

The NCLT route is the standard process. The fast-track route under Section 233 is available to eligible companies and bypasses the NCLT completely. Both follow a defined sequence; deviation from it creates procedural grounds for objection.

Step 1: Board Approval

Board resolutions approving the scheme are required from both the Demerged Company and the Resulting Company. Each resolution needs to record the commercial rationale, structure, and key terms of the demerger.

Step 2: Drafting the Scheme of Arrangement

The scheme covers assets, liabilities, contracts, employees, and licences being transferred. It sets out the share entitlement ratio, conditions precedent, the effective date, and the consequence of approvals not coming through. This is the document everything else rests on. Errors in it are not easy to fix once the process is underway.

Step 3: Stock Exchange and SEBI NOC (Listed Companies Only)

Listed companies have a mandatory pre-step before the first NCLT filing. A No Objection Certificate from the stock exchanges and compliance with SEBI disclosure requirements must both be in place first. This requirement comes from the SEBI Master Circular dated 20th June 2023.

Step 4: First Motion Application to NCLT

The Demerged Company and Resulting Company file a joint application. The NCLT issues directions for meetings of shareholders and creditors.

Step 5: Shareholder and Creditor Meetings

The scheme needs approval from a majority representing at least three-fourths in value of members and creditors present and voting at each class meeting.

Step 6: Second Motion Petition

After successful meetings, the second motion petition is filed with meeting results, newspaper advertisements, and responses from the Regional Director, Registrar of Companies, Official Liquidator, and Income Tax Department.

Step 7: NCLT Sanction Order

The NCLT goes through the scheme on two counts: fairness and compliance. A sanction order under Section 232 follows if it is satisfied. For sector-regulated companies, that order does not become effective until RBI, SEBI, IRDAI, or TRAI approvals are also secured.

Step 8: Filing with the Registrar of Companies

A certified copy of the NCLT sanction order must be filed in Form INC-28 within 30 days. The demerger is legally effective upon this filing.

Step 9: Post-Demerger Implementation

Asset transfers, shareholder record updates, licence transfers, tax filings, and SEBI disclosures do not happen automatically. They are each governed by the terms of the approved scheme and need to be executed accordingly.

What Has Changed with the CAA Amendment Rules, 2025?

The CAA Amendment Rules, 2025, are the most significant liberalisation of India’s restructuring framework since the original CAA Rules in 2016. For strategic demergers specifically, the changes resolve a long-standing ambiguity and expand the range of companies that can use the faster, cheaper route.

Two things matter most.

First, the 2025 Amendment inserted a new sub-rule (9) in Rule 25, explicitly confirming that the fast-track procedure applies to demergers, divisions, and transfers of undertaking. Before this, practitioners were working around an interpretational gap. That gap is now closed.

Second, the eligibility for the fast-track route has been significantly widened. The following can now use it:

- Two or more unlisted companies with outstanding borrowings not exceeding Rs. 200 crore and no loan defaults, subject to auditor certification

- A holding company (listed or unlisted) and its unlisted subsidiary

- Two or more unlisted subsidiaries of the same holding company

Why does this matter? The fast-track route bypasses the NCLT entirely. Approval comes from the Regional Director with jurisdiction over the Transferee Company. That is substantially faster and cheaper than an NCLT process that, as of March 2025, had approximately 15,000 cases pending across mergers, insolvency, and company law petitions. For group restructurings that previously had no alternative to the NCLT queue, the 2025 Amendment is a genuine change.

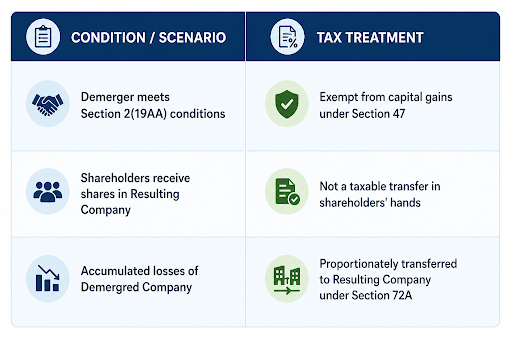

How Are Strategic Demergers in India Treated for Tax Purposes?

A demerger that meets the Section 2(19AA) conditions is tax-neutral. The transaction does not attract capital gains at the company level or in the hands of shareholders. Miss any of the conditions and the tax-neutral status is lost entirely.The four conditions for Section 2(19AA) compliance are non-negotiable:

- All property and liabilities of the undertaking must vest in the Resulting Company

- Property must be transferred at book value net of accumulated depreciation

- The Resulting Company must issue shares to shareholders of the Demerged Company on a proportionate basis

- Shareholders holding at least three-fourths in value of shares in the Demerged Company must become shareholders of the Resulting Company

A single deviation from any of these removes the tax-neutral status. The transaction then attracts capital gains in the hands of the company and its shareholders. At the planning stage, the scheme structure must be mapped against each condition before drafting begins.

What Are the Practical Challenges in Executing Strategic Demergers in India?

The framework is clearer now than it has ever been. The execution challenges have not changed.

Regulatory Coordination

Demergers involving regulated businesses need approvals from sector regulators, RBI for financial services, TRAI for telecom, that do not follow the NCLT or the Regional Director timeline. These must be tracked in parallel, not treated as post-sanction clean-up.

Licence and Contract Transfer

Business licences and commercial contracts do not automatically vest in the Resulting Company in all cases. Some require fresh applications or third-party consents. Missing these at the drafting stage means discovering them after the sanction order is in hand, which is an expensive problem.

Valuation and Share Exchange Ratio

The share entitlement ratio must be based on a fair valuation by an independent registered valuer. Disputes over the ratio are consistently among the most common sources of delay. A ratio that looks internally justifiable but is not independently supportable invites shareholder objections.

Minority Shareholder Objections

The NCLT process provides a formal window for dissenting shareholders and creditors to challenge the scheme. The practical defence against successful objections is straightforward: clear disclosure and a commercial rationale that is properly documented.

Employee Transfer

Employees of the transferred undertaking become employees of the Resulting Company once the scheme is approved. Service continuity, existing terms, and protections under the Industrial Disputes Act, 1947, and applicable State labour codes must be maintained. Handling this poorly at the communication stage creates employee attrition in the months surrounding the demerger.

Conclusion

Strategic demergers in India have become a mainstream restructuring tool. The CAA Amendment Rules, 2025, made the fast-track route accessible to a much larger set of companies. The tax framework under Section 2 (19AA) is well-established when the conditions are met. The NCLT process, while slower, is structured and predictable for transactions that cannot use the fast-track route.

What determines outcomes is execution quality. A scheme that is structurally sound but imprecisely drafted, built on a valuation that cannot withstand scrutiny, or sequenced without accounting for sector regulator timelines, will encounter delays regardless of how clean the underlying transaction is.

CorporateLegit advises businesses across every stage of strategic demergers in India, from scheme drafting and NCLT filings to post-demerger compliance, regulatory approvals, and tax structuring. If your business is evaluating a demerger, reach out to CorporateLegit at the planning stage, not after the first filing is made.

FAQs

Q1. What is the difference between a demerger and a spin-off in India?

In Indian legal terminology, a spin-off and a strategic demerger in India refer to broadly the same transaction, where a portion of a company’s business is transferred to a separate entity. The term “demerger” is the legally recognised term under Section 2(19AA) of the Income Tax Act and Sections 230 to 232 of the Companies Act, 2013. A spin-off is a commercial term. The legal mechanism used in India is always the scheme of arrangement approved by the NCLT or, for eligible companies, by the Regional Director under the fast-track route.

Q2. Can a private limited company in India undertake a strategic demerger?

Yes. Strategic demergers in India are not limited to listed companies. Private companies can undertake demergers under Sections 230 to 232 of the Companies Act, 2013, or through the fast-track route under Section 233 if they meet the eligibility criteria. Following the CAA Amendment Rules, 2025, unlisted companies with borrowings up to INR 200 crore and no loan defaults can now access the fast-track demerger route, which is considerably faster and less expensive than the NCLT process.

Q3. How long does a strategic demerger in India typically take?

The timeline for strategic demergers in India depends on the route taken. An NCLT-routed demerger typically takes 12 to 24 months, factoring in scheme preparation, NCLT hearings, shareholder meetings, and post-order filings. The NCLT’s significant case pendency has contributed to extended timelines. Under the fast-track route available for eligible companies after the CAA Amendment Rules, 2025, the timeline can be reduced to 4 to 6 months, subject to Regional Director processing.

Q4. What happens to existing employees when a demerger is executed?

Employees of the transferring undertaking become employees of the Resulting Company by virtue of the approved scheme. Their service continuity, seniority, and existing terms of employment are preserved. The Resulting Company assumes all employment liabilities. Any adverse change to employee terms without following due process under applicable labour laws creates statutory liability. Proper communication and documentation of the transfer is mandatory and must be completed promptly after the scheme becomes effective.

Q5. Is a strategic demerger in India taxable for shareholders?

Provided the demerger satisfies the conditions under Section 2(19AA) of the Income Tax Act, 1961, the transaction is tax-neutral for both the company and its shareholders. Shareholders receive shares in the Resulting Company without any capital gains liability arising on receipt. The cost of acquisition and period of holding of the original shares in the Demerged Company are apportioned between the shares held in the Demerged Company and the shares received in the Resulting Company, in proportion to the net book values of the transferred and retained undertakings.