EdTech Company Setup in India: FDI, GST and Regulatory Requirements

Introduction

India’s EdTech sector went through a dramatic cycle in the space of five years. Between 2020 and 2022, it attracted over USD 8 billion in funding, produced multiple unicorns, and was treated as one of the highest-growth consumer internet opportunities in the world. Then came the correction. BYJU’S ran into well-documented financial and regulatory trouble. Several mid-tier EdTech companies shut down or severely cut back. Investor appetite tightened.

What remained after the correction is a sector with genuine long-term fundamentals. India has 500 million-plus internet users, over 250 million students in formal education, a massive skill development gap in the workforce, and state and central government programmes actively pushing digital education. The EdTech opportunity in India is real. What changed after 2022 is that investors and founders now expect the business model to be financially sound and the regulatory compliance to be clean.

EdTech company setup in India is operationally simpler than most regulated sectors. There is no sector-specific licence for online education. But there are GST complexities, FEMA compliance for foreign investment, data protection obligations under DPDPA 2023, and consumer protection requirements that apply to the first subscriber.

What FDI Rules Apply to EdTech Company Setup in India?

100% FDI is permitted in an EdTech company setup in India under the Automatic Route. There is no sector-specific cap, no government approval requirement, and no minimum capitalisation condition. EdTech sits within the broader education sector, where FDI policy has been progressively liberalised.

The education sector previously had restrictions on FDI, particularly for formal education institutions like schools and universities. Those restrictions were substantially relaxed, and for EdTech companies operating as technology or service platforms, 100% FDI under the Automatic Route has been the position for several years.

There is one classification question that matters here. An EdTech company operating as a technology platform providing online courses, skill development content, or test preparation services is treated as a technology or services company for FDI purposes. A company operating a formal school or university is subject to different considerations. Most investors and founders are in the technology platform category, which is where 100% Automatic Route FDI applies cleanly.

FDI in EdTech India triggers standard FEMA reporting obligations. Form FC-GPR goes on RBI’s FIRMS portal. The deadline is 30 days from the date of share allotment. Documents needed: FIRC from the bank, investor KYC, valuation certificate from a SEBI-registered Merchant Banker or CA, and a Board Resolution approving the allotment. Miss the 30-day deadline, and a Late Submission Fee kicks in. Multiple missed rounds accumulate into a compounding matter that must be resolved before the next transaction.

What Legal Structure Should an EdTech Company Use in India?

A Private Limited Company is the right structure for an EdTech company setup in India. Equity funding works cleanly with this structure. So do ESOPs and foreign investment through the standard FEMA framework.

This is not a difficult decision for most EdTech founders. The sector is venture-backed, ESOPs matter for hiring engineers and content creators, and the Private Limited structure supports equity fundraising cleanly at every stage. None of these works with an LLP or sole proprietorship.

For foreign companies setting up an India EdTech operation, a Wholly Owned Subsidiary incorporated as a Private Limited Company allows 100% ownership, profit repatriation after applicable taxes, and a clean intercompany structure for technology licensing or content licensing arrangements with the parent entity. Those licensing arrangements immediately create transfer pricing obligations, which is something foreign-backed EdTech companies need to plan for from the first intercompany invoice.

How Does GST Apply to an EdTech Company Setup in India?

GST treatment of EdTech services in India is genuinely complex and has been the subject of multiple clarifications. The rate depends on the nature of the service: education as such is exempt, but most EdTech services attract 18% GST.

This distinction has caused real compliance problems in the sector.

Services provided by an educational institution to its students are exempt from GST. But an EdTech platform is not an educational institution for GST purposes unless it is recognised by law as one. Online courses sold by a private EdTech company, test preparation subscriptions, skill development programmes, and corporate training services all attract 18% GST.

There are two categories of EdTech services that have received specific GST treatment:

Recorded online courses: 18% GST applies.

Live online classes: If the online education services are conducted live and are effectively equivalent to classroom teaching, some GST rulings have treated these differently depending on the specific facts. This is an area where the GST position must be confirmed with a tax adviser for each product type before invoicing begins.

Export revenue changes the GST picture for an EdTech company setup in India. Services delivered to learners outside India, with payment received in foreign currency, can qualify as zero-rated under Section 16 of the IGST Act. A Letter of Undertaking (LUT) must be filed on the GST portal before the first export invoice to avoid collecting GST upfront and then claiming a refund.

The RBI purpose code for EdTech services provided to foreign customers is important. Education-related services typically fall under purpose code P0102 (education-related travel) for physical movement or S0208 (educational services) for cross-border digital services. Using the wrong purpose code at the bank creates complications in GST refund claims and FEMA reporting.

What Data Protection Obligations Apply to EdTech Companies in India?

The Digital Personal Data Protection Act, 2023 (DPDPA) applies to every EdTech company processing personal data of individuals in India. For EdTech platforms serving children and students, the obligations are more stringent than for general consumer apps.

EdTech platforms sit on substantial personal data. Names, ages, learning progress, assessment results, payment details, and for platforms using proctoring solutions, biometric data on top of that. Under DPDPA:

- Explicit, purpose-specific consent must be obtained before collecting personal data.

- Consent has to be explicit and tied to a specific purpose, collected before the data, not after.

- For children’s data, parental consent needs to be verifiable. Using that data for tracking, behavioural monitoring, or targeted advertising is not permitted under any circumstances.

- Security safeguards are not one-size-fits-all. They have to match the volume and sensitivity of what is being held.

- Data breaches go to the Data Protection Board of India. There is no internal handling option.

- Users can access, correct, and erase their data. That is not a feature; it is a legal right.

For an EdTech company setup in India targeting K-12 students, the children’s data provisions are not a peripheral concern. Student learning data has one permitted use: delivering the educational service. Advertising, profiling, and selling to third parties any of that creates DPDPA exposure.

What Consumer Protection Requirements Apply to EdTech Companies?

The Consumer Protection (E-Commerce) Rules, 2020, and the Consumer Protection Act, 2019, apply to EdTech platforms. Course refund disputes, misleading placement guarantees, and subscription cancellation issues have been active areas of consumer complaints in the EdTech sector.

The Consumer Protection Act, 2019, introduced the concept of product liability and significantly strengthened consumer rights. For EdTech platforms, the specific areas of regulatory attention have been:

Misleading advertisements: Platforms making placement guarantees or income projections that cannot be substantiated have attracted notices from the Central Consumer Protection Authority (CCPA). Any marketing claim about job placement rates, salary outcomes, or course completion benefits must be verifiable.

Unfair contract terms: Subscription agreements that make cancellation difficult, that automatically renew without clear notice, or that impose disproportionate penalties for early termination have been challenged under the Consumer Protection Act.

Grievance redressal: A Grievance Officer is mandatory. Name and contact details go on the platform, visible to users. Complaints get acknowledged within 48 hours and resolved within 30 days.

What Are the Steps for EdTech Company Setup in India?

The process for EdTech company setup in India is sequential. Companies Act incorporation first, then GST registration, and DPDPA compliance, all before the product goes live.

Incorporation goes through SPICe+ on the MCA portal. One thing that gets missed often: the MoA objects clause needs to describe EdTech and online education activities specifically. Generic entries like “e-commerce” or “technology services” are not enough. INC-20A comes next, and it has to be filed within 180 days of incorporation, before the first user is onboarded. Register for GST before raising the first invoice. File the LUT before the first export invoice if serving overseas learners.

Build the DPDPA consent framework into the product from the MVP stage. Adding it later is technically complicated and operationally disruptive. For platforms serving students under 18, build the parental consent mechanism into the onboarding flow from day one.

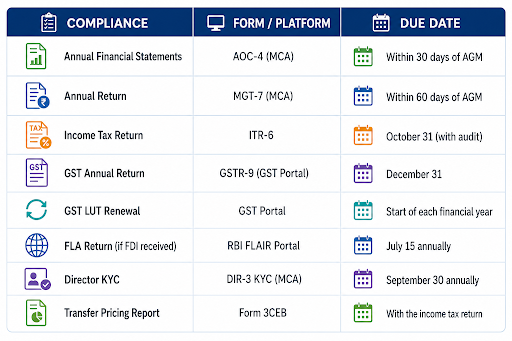

Annual Compliance Calendar Conclusion

An EdTech company setup in India does not require a sector-specific licence. That makes it easier to start than a healthcare or financial services business. What it does require is a GST position confirmed before the first invoice, DPDPA compliance built into the product before the first user, consumer protection obligations understood before the first marketing campaign, and FEMA reporting maintained from the first foreign investment received.

The EdTech sector in India had its reckoning between 2022 and 2024. The companies that survived and grew through that period were the ones where the compliance and governance foundations were solid. That is not a coincidence.

CorporateLegit handles EdTech company setup in India from incorporation to GST and LUT filing, FEMA compliance, transfer pricing framework design, and ongoing annual compliance. If you are building an EdTech business in India and want the regulatory foundation right from the start, reach out to CorporateLegit.

FAQ

1. Is 100% FDI allowed for EdTech company setup in India?

Yes. EdTech platforms operating as technology and services companies attract 100% FDI under the Automatic Route. No prior government approval is required. Post-investment, Form FC-GPR must be filed on RBI’s FIRMS portal within 30 days of share allotment.

2. What GST rate applies to EdTech services in India?

Most EdTech services including recorded online courses, test preparation subscriptions, skill development programmes, and corporate training attract 18% GST. Services by a recognised educational institution to its students are exempt, but private EdTech platforms generally do not qualify for this exemption. The exact rate for each product type should be confirmed with a tax adviser before invoicing begins.

3. How does the LUT work for EdTech companies with foreign customers?

A Letter of Undertaking allows an EdTech company to invoice foreign customers without collecting GST upfront, treating the supply as a zero-rated export of services. The LUT must be filed on the GST portal before the first export invoice and renewed at the start of each financial year. Payment must be received in foreign currency for the zero-rating to apply.

4. What DPDPA obligations apply specifically to EdTech platforms?

EdTech platforms must obtain explicit consent before collecting personal data, implement proportionate security safeguards, report breaches to the Data Protection Board, and honour user rights including erasure requests. For platforms serving students under 18, verifiable parental consent is required and behavioural tracking or targeted advertising of children is prohibited.

5. What are the consumer protection obligations for EdTech companies?

EdTech platforms must appoint a Grievance Officer, acknowledge complaints within 48 hours, and resolve them within 30 days. Marketing claims including placement guarantees and salary projections must be substantiated. Subscription terms must be fair and clearly communicated. The Consumer Protection Act, 2019 and the Consumer Protection (E-Commerce) Rules, 2020 both apply.

6. What transfer pricing obligations apply to foreign-backed EdTech companies in India?

All intercompany transactions between the Indian EdTech entity and its foreign parent or related entities, including technology licensing fees, content licensing, management charges, and brand royalties, must be priced at arm’s length under Sections 92 to 92F of the Income Tax Act. Form 3CEB must be filed with the income tax return for entities with international transactions above Rs. 1 crore.